Death and Taxes

You may have heard this phrase: “there are only two guarantees in life: death and taxes.” What’s more, many times, taxes are guaranteed upon death, especially if there is a sizeable estate. Even with a small or medium sized estate, sometimes the government gets a real windfall in taxes, where there is little or no proactive estate planning already done.

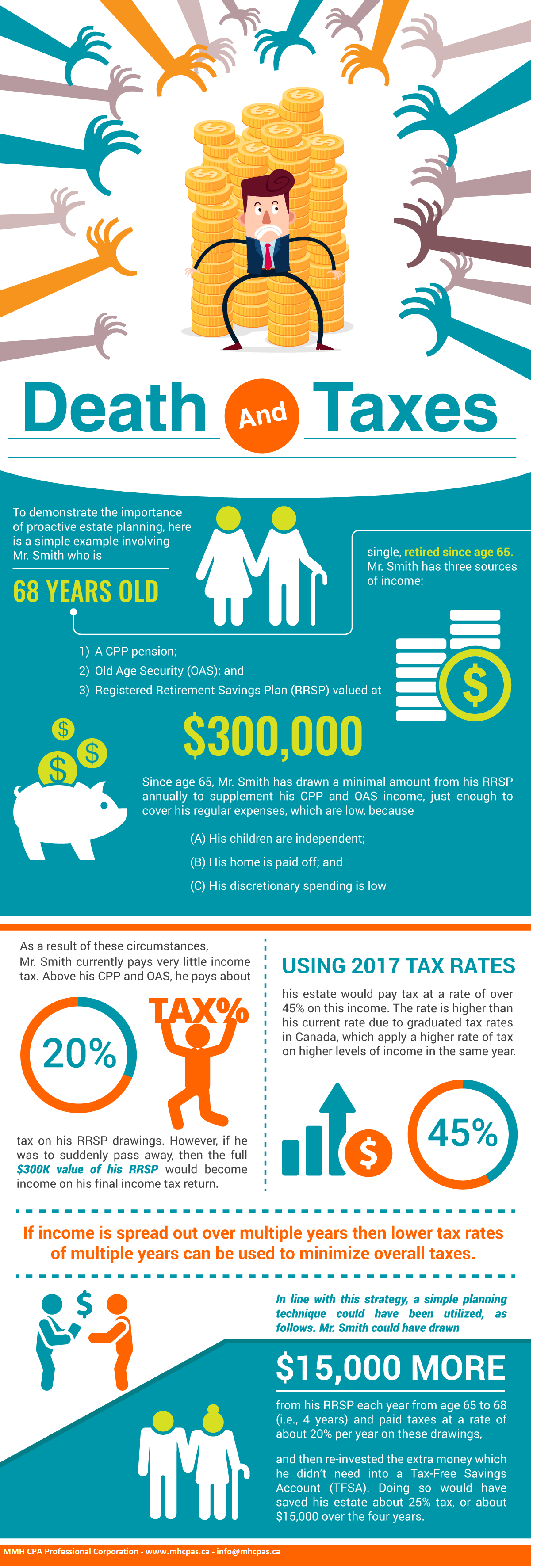

To demonstrate this point, I will provide a simple example. See below for illustrated version. This example involves Mr. Smith who is 68 years old, single, retired since age 65. Mr. Smith has three sources of income: a CPP pension, OAS (Old Age Security), and a Registered Retirement Savings Plan (RRSP) valued at $300,000. Since age 65, Mr. Smith has drawn a minimal amount from his RRSP annually to supplement his CPP and OAS income, just enough to cover his regular expenses, which are low, because (a) his children are independent; (b) his home is paid off; and (c) his discretionary spending is low.

As a result of these circumstances, Mr. Smith currently pays very little income tax. Above his CPP and OAS, he pays about 20% tax on his RRSP drawings. However, if he was to suddenly pass away, then the full $300K value of his RRSP would become income on his final income tax return. Using 2017 tax rates, his estate would pay tax at a rate of over 45% on this income. The rate is higher than his current rate due to graduated tax rates in Canada, which apply a higher rate of tax on higher levels of income in the same year.

If income is spread out over multiple years then lower tax rates of multiple years can be used to minimize overall taxes. In line with this strategy, a simple planning technique could have been utilized, as follows. Mr. Smith could have drawn $15,000 more from his RRSP each year from age 65 to 68, inclusive, (i.e., 4 years) and paid taxes at a rate of about 20% per year on these drawings, and then re-invested the extra money which he didn’t need into a Tax-Free Savings Account (TFSA). Doing so would have saved his estate about 25% tax, or about $15,000 over the four years.

While this example is meant to demonstrate the consequences of poor planning in simple terms, actual figures could vary depending on the specific facts. Of course, real life is not necessarily simple. There are many facts and circumstances that could change the plan and strategy. Unlike Mr. Smith, you might not be single; or you might have dependent children; or you might have higher income; you could already have a TFSA with the maximum amount of room used up already; or you might own a business or property. In each of those circumstances, a different strategy or strategies would optimal. The point is that it is better to plan ahead as much as you can and to utilize expertise where needed, so that, as a silver lining for your death, your family which you leave behind gets the windfall, and not the government!

Looking for an expert? Contact Us today!

Attaul Hamid

Disclaimer:

The contents of this article are written and published to provide general information and are not intended to substitute advice. As individual circumstances, which may be applicable in a specific situation, have not been addressed in this article, readers seeking specific advice may find the information misleading. Such readers are encouraged to consult a professional to obtain complete and relevant advice related to their situation. We have made every effort to prepare the information with care. However, we do not accept responsibility for its use and any outcome arising out of its use. Where opinions are expressed, such opinions do not reflect the facts of the subject matter and should not be considered as advice or recommendation(s).